Indonesia Emerges as Key Cobalt Supplier, Challenging DRC Dominance, IEA Report Shows

Global – The International Energy Agency’s (IEA) “Global Critical Minerals Outlook 2024,” released on May 17, 2024, highlights Indonesia’s rapid ascent as a major player in the global cobalt supply chain, significantly impacting the traditional dominance of the Democratic Republic of Congo (DRC). The report details how Indonesia has become the world’s second-largest cobalt supplier, driven by its burgeoning nickel industry.

The IEA report emphasizes that Indonesia’s cobalt production has seen a remarkable twenty-fold increase in the last four years, a surge directly linked to the Indonesian government’s nickel ore export ban, which spurred investments in domestic nickel-cobalt processing operations, particularly High-Pressure Acid Leaching (HPAL) facilities. This policy shift led to a flood of investments, transforming Indonesia into a key cobalt supplier.

According to the IEA, Indonesia’s cobalt production is projected to more than double by 2030, reaching 50 kt in the base case scenario and potentially 80 kt in the high production case, constituting 23% of global cobalt supply and significantly reducing the DRC’s market share. The report notes that Indonesia’s rise is driven by the production of mixed-hydroxide precipitate (MHP) from its HPAL facilities.

Key points from the IEA report regarding Indonesia’s role in the cobalt market include:

- Rapid Growth: Indonesia’s cobalt production has increased twenty-fold in the last four years.

- Second-Largest Supplier: Indonesia is now the world’s second-largest cobalt supplier.

- HPAL Facilities: Investments in HPAL facilities are a major driver of Indonesia’s increased cobalt production.

- Projected Increase: Indonesia’s cobalt production is expected to more than double by 2030.

- Nickel Connection: The rise in cobalt production is tied to Indonesia’s expanding nickel industry, as cobalt is often extracted as a by-product of nickel ore.

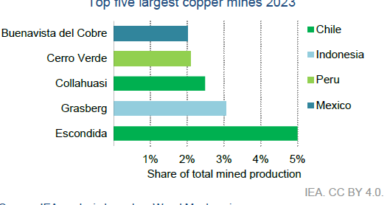

The IEA notes that while the DRC remains the largest supplier of mined cobalt, with a 65% market share in 2023, its dominance is being challenged by Indonesia. The report also points out that the DRC’s cobalt production may decline in the long term due to diminishing ore grades and increasing production costs, necessitating the exploration of new deposits, re-evaluation of old tailings, or a shift from open-pit to underground operations.

The report also underscores that Indonesia’s rise in cobalt production is changing the landscape of the global supply chain. The country’s growing role in cobalt is closely linked to its nickel sector, as cobalt is often extracted as a by-product of nickel mining. Nickel plays a growing role as a primary mineral for cobalt production, with its share rising to almost 40% by 2040.

The IEA also mentions that the rise of HPAL facilities in Indonesia, while boosting cobalt production, also raises concerns over the environmental impacts of these operations and their reliance on coal-powered facilities for their energy needs. The report highlights a trade-off between lower emissions intensity of HPAL vs. waste production from the process.

The IEA report suggests that this shift in cobalt production, with Indonesia becoming a key player, has significant implications for the market, including potential shifts in pricing, supply security, and the environmental impacts of mineral extraction.

Historically, the DRC has been the dominant force in the cobalt market, with the majority of the world’s cobalt sourced from its copper-cobalt mines. However, Indonesia’s emergence as a major cobalt producer marks a significant shift in the global landscape, creating a more diversified supply base and bringing new challenges and opportunities for the industry. The IEA’s analysis underscores the critical need for stakeholders to adapt to this changing landscape and address the associated environmental and social concerns.